Arizona prices remained high in the last quarter of 2024, despite slight declines over the past two years. As of December, home prices in the state were just 6.1% below their all-time peak set in July 2022, while prices in the Phoenix Metro are 7.3% below their peak. Today, the average home in Arizona costs $424,800; in 2019, it cost $267,700.

As a result, sales of existing homes in the western region of the country remain near the lows of the last two years, and the rate of sales of existing homes as of December 2024 is down 36% from the rate experienced in 2021.

[i] Meanwhile, new homes for sale have increased 28% over the same period, but the volume is insufficient to offset the loss of existing sellers.

Mortgage Affordability

The average 30-year mortgage rate in December 2024 was 6.72% (+0.54 percentage-points since September 2024). The average price of a home in Arizona is $425,600. Given those figures, a typical monthly mortgage payment would cost $2,201. This is roughly unchanged over the past year. In December 2019, a typical 30-year mortgage would have had a monthly cost of $1,019.

To afford a house in today’s market under conventional mortgage guidelines, Arizonans would need an annual income of $109,500. Alternatively, at the average hourly wage rate of $34.37, the typical household in Arizona would need to work 64 hours/month (over one-and-a-half weeks) to service the average mortgage payment.

Permitting & Supply

In 2024 Q4, Arizona’s local jurisdictions issued 12,866 residential building permits (-14.7% from Q3 2024 and -16.6% from Q4 2023). For the entire year, the state is on track to approve construction of 59,306 housing units – in increase of 1.7% from 2023 and an increase of 27.3% from 2019.

The 2024 permitting level is more than the states average permitting pace over the last 10 years of 47,600 annually. However, permit activity peaked in 2022 at 61,084 residential permits and has been slowing since.

New home construction and permit activity surged between 2020 and 2022, following pandemic-era price spikes. However, as with the U.S. more broadly, permitting fell in Arizona towards the end of 2022, and only briefly recovered before falling again in late 2024. A total of 3,275 residential building permits were issued in December 2024. At its recent peak (March of 2022) Arizona issued nearly 6,800 permits. The current pace of permitting is not enough to keep up with pent-up demand and resolve the housing shortfall.

While not all permits result in housing units, Permitting activity provides an insight into the pace of new homes entering the market with about a 1 year lag. On average, 91% of housing permits turn into housing units over the next year. Based on the number of housing permits in 2024, Arizona is not on track to build enough housing units to close the deficit. In order to keep up with population growth and growing housing demand, Arizona would have to add around 50,000 housing units annually; CSI forecasts 49,700 units over the next year.

While the housing shortage did shrink in late 2024, it is more attributable to rising vacancy rates as people leave the housing market after being frustrated by high prices and borrowing costs, rather than increasing supply.

As discussed in prior CSI reports, there is a large gap between the mortgage rates possessed by current homeowners (who bought when rates were much lower) and the market rates available to current buyers. This creates a mortgage lock-in effect – a phenomenon where homeowners are reluctant to sell their current home and buy another due to higher mortgage costs. As a result, the number of housing transactions plummeted from pre-pandemic levels, and new homes as a share of all homes for sale increased 22.5 percentage points between 2019 and 2024 - as of January 2025, nearly half of all homes for sale are new.

[ii] The number of U.S. homes for sale has decreased 5% from their 2022 peak, while new homes for sale are at an all time high and up 5% over the previous 2022 peak.

In summary, the housing market today is more dependent on new-construction than it has been historically – especially at the lower-end of the market. New construction is costly and slow to bring to market, in part due to local building codes and permitting restrictions.

Arizona’s Housing Shortfall

To assess the pace of permitting, new construction, and overall additions to Arizona’s housing supply in meeting the demands of buyers, CSI Arizona utilizes two measures: a market-based “instantaneous” estimate of the real-time gap between supply and demand informed by vacancy rates, and a housing-supply-focused “cumulative” measure that is slower and less responsive to demand changes but tracks longer-term growth in the housing supply relative to underlying population growth and household formation. The market-based measure captures demand changes when discouraged folks exit the housing market by, for example, living with parents or roommates for longer. The cumulative deficit does not account for this and assumes long-term housing growth must keep up with long-term population growth and historical housing formation rates. For completeness, both results are reported here as a range.

On a real-time basis, currently, CSI estimates an instantaneous housing shortfall of 56,616 units in 2024, down 17% from the revised shortfall of 68,658 in 2023. While this decline reflects the uptick in both home permitting and home-building after 2020, it also reflects the collapse in demand as rising prices and interest rates have driven consumers out of the market for homes. This estimate holds given the current state of the market (and particularly continued-high market interest rates coupled with relatively-low-rates for existing homeowners).

Alternatively, CSI’s supply-driven “cumulative” estimate of the housing shortfall as of 2024 shows an Arizona housing deficit of 240,760 units. This larger shortfall tracks the tepid growth in housing units in the state relative to the growth in population and other benchmarks, cumulatively and over time. This provides some insight into the state’s likely longer-term needs, if prices and interest rates normalized and more households were drawn into the housing market.

Although these estimates always differ, they have moved in opposite directions over the last couple years. This divergence illustrates a point we have made throughout this piece: any improvement in the contemporary Arizona housing market is characterized more by a lack of buyers at current prices and interest rates than an increased home supply. Given the number of permits issued in 2024, it would take the state 13 years to close just the “instantaneous” housing deficit. The state has made no meaningful progress in addressing its pent-up “cumulative” shortfall since 2022.

The Local Housing Shortage

As a reminder: Arizona local jurisdictions – cities, towns, and counties – are responsible for issuing residential building permits. They also determine local building codes, architectural and design requirements, and code and permit enforcement. Therefore, it is especially helpful to review local and regional housing supply conditions, versus purely statewide perspectives. But data availability issues make the consistent technical calculation of these indicators at the city-level difficult, and household freedom of movement – people can choose where they live and ultimately move to places that are building housing and especially affordability housing – make doing it difficult. CSI attempts to address both issues by relying on a mix of local and county-wide data, as available, and holding each city to the standard of its

county population growth rate (rather than its local city-level population growth rate). So, for example, Scottsdale is held to Maricopa County’s population growth rate when assessing its pace of permitting against growth-driven need, instead of its own (slower) growth rate, because we assume Scottsdale is growing more slowly in part

because it lacks (affordable) housing.

11 of the 15 counties in Arizona had an (“instantaneous” or market-indicated) housing deficit in 2024. Out of those with a deficit, Navajo County has the largest as a share of its total existing housing units (2.97%), while Gila County (0.46%) has the lowest. Maricopa County – the state’s largest county by population – has a projected deficit of 37,744 units, or 1.94% of the existing housing stock.

In the state’s largest county, the housing deficit appears to be growing following a dip in permitting activity. According to Census data, Maricopa County issued 36,011 permits in 2024, which translates to an estimated 32,770 new housing units this year – roughly 2,000 less than the number from 2023. CSI estimates the county would need to build 32,600 units a year just to keep pace with population growth, leaving only 260 new units annually to contribute to lowering the current deficit of 37,744 housing units. At this pace of permitting, CSI estimates it would take Maricopa County over 150 years to close their current housing shortfall.

While U.S. Census and other sources provide good data about housing supply and households at the countywide-level, Arizona’s 90 cities and towns issue the vast majority of the states building permits.

Because of this, CSI begun individual assessing how well these jurisdictions are performing in permitting and building new housing units, despite a relative lack of data. CSI estimates the housing deficit of each jurisdiction based on their respective vacancy rates and the grade is based on how well they are permitting relative to their population growth rate of their respective counties. To summarize, where available, this analysis uses city-level data; where not, we rely on county-level data prorated to that city or town.

79 of the 90 cities and towns in Arizona had a housing deficit in 2023. Chino Valley in Yavapai county had the largest deficit as a share of its total existing housing units (5.1%), while Safford in Graham county (0.1%) has the lowest. Phoenix – the state’s largest city by population – has a projected deficit of 17,884 units, or 2.8% of the existing housing stock.

According to Housing and Urban Development data, Phoenix – Arizona’s largest city - issued 14,468 permits in 2023, which translates to an estimated 13,165 new housing units in 2024. CSI estimates the city would need to issue 11,812 permits a year just to keep pace with population growth, leaving 2,655 new permits annually to contribute to lowering the current deficit of 17,884 housing units. At this pace of permitting, CSI estimates it would take Phoenix 7 years to close their current housing shortfall.

Tucson, Arizona’s second largest city, has a deficit of 4,866 housing units and only issued 1,668 permits in 2023. In order to keep up with population growth, Tucson would need to permit for 2,667 units annually. At this pace of permitting and population growth, Tucson would never close their housing deficit.

Mesa, Arizona’s third largest city, has a deficit of 5,689 units and needs to issue 4,063 permits annually to keep up with the population growth. With only 2,162 permits issued from Mesa in 2023, the city is not on pace to ever close its housing shortage.

Sedona – on the other end as one of Arizona’s smaller, rural towns - presents an interesting case. With a population of less than 10,000 and just 6,822 housing units, it is one of the smallest cities in Arizona. But with an average home price of $497,000 – 17% higher than the statewide average – it is one of the more exclusive and expensive places to buy a home. Reflecting the unaffordability of the city’s existing housing stock, “instantaneous” demand is low and vacancy rates (5.2%) relatively high – undercutting the argument that short-term-rentals, and not overall affordability and supply issues, are driving the city’s housing issues, and instead reflecting buyer pessimism. Still, the “cumulative” shortfall (215 units) reflects the paucity of development here. Given expected population and demand growth and the tepid pace of permit issuances, the city is on track not even to keep pace with that natural demand and never resolve its underlying structural issues.

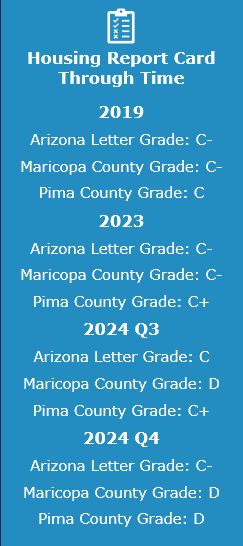

Arizona’s Housing Report Card

CSI Arizona debuted its inaugural version of the state’s Housing Report Card in May 2024 – which considering housing market data through Quarter 1 2024. At the time, the state earned an average “C+” letter grade for the overall performance of its local housing markets across four measures of price and supply: cumulative housing price increases, rent to household income ratio, people-per-housing unit, and permitting-to-shortfall ratio.

Since then, the decline in permitting has more than offset any other improvements in local conditions, and the statewide average grade has fallen to a “C-”. Given current trends, homebuilding is likely to continue slowing in the short term, unless permitting trends change quickly and dramatically.

Housing Report Card Methodology

This methodology relies on national statistical data collected by various Federal agencies, allowing CSI to develop a consistent and objective grading rubric for Arizona’s fifteen counties (as geographic areas, not political entities) and statewide conditions. While the letter grades apply to the counties and the state, they should not be interpreted as scores of the County or State governments themselves. Instead, local permitting jurisdictions – typically a City or Town, but occasionally the local County government – have the most immediate influence over the ability of developers and builders to rapidly and affordably bring to market the types of housing people are willing to buy. The more restrictive these local development and permitting processes, the slower newer housing comes to market, and the more expensive it may be.

To assess these processes, CSI measured local performance across the four subject areas – cumulative price increases since 2020, rent-to-income ratios, the number of people-per-housing unit, and the pace of home permitting relative to its housing needs – relative to national and long run norms. A weighted average of these four units produces the area’s final overall grade. Because this index is intended to primarily assess how permissive to development a region is, we double weight the pace of home permitting relative to an area’s housing needs.

For each metric, all counties and the state were compared to the national average plus or minus a set number of standard deviations to yield the letter grades. Areas more than a full standard deviation below the national average received a 4.0 (A); one standard deviation below to 0.33 standard deviations above 3.0 (B); 0.33 standard deviations above to one full standard deviation above 3.0 (C); between one and two standard deviations above 1.0 (D); and higher than two standard deviations 0.0 (F).

Cumulative price increases: Areas were graded on their cumulative price increases since 2000 relative to the national average of 194.4% growth. Areas with less than 138% growth (one full standard deviation below average) earned an A, while areas with price growth exceeding 307% (two full standard deviations above the national average) received an F.

Rent-to-Income Ratio: Rent-to-income ratios for each area were compared to the national average of 20.4%. Counties with ratios below 17.21% earned an A grade, with counties over 26.83% earning an F.

People-per-housing unit: The average number of people-per-household in the U.S. was 2.35 in 2023. Counties with less than 2.19 people per household received an A, and counties over 2.67 people per household received an F.

Permitting to shortfall: Counties and the state were compared to the historical average time a county would take to close its housing given historical permitting rates. Counties that were estimated to take less than 3.7 years to close their deficit earned an A, while counties exceeding 58.1 years earned an F.

Figure 10 below provides an example of the grading for the pace of home permitting relative to each area’s housing needs. The more permits an area issues the shorter the time frame to close the estimated housing deficit – all else equal – which results in a higher letter grade.

Appendix A: City Housing Shortage

Because of data availability limitations, CSI cannot replicate complete scorecards (and aggregate letter grades) for all of Arizona’s cities or towns. We can only grade all cities and towns on the Housing Shortfall component of the Report Card, and this performance is presented in full in Appendix A.