Summary Findings

- In the first year following the passage of TABOR, fee-based enterprises generated $742 million. By 2023, their revenue had increased by over 3,000%, far beyond population growth (62%), to $23.3 billion.

- In 1996, only 46% of total state spending was TABOR-exempt—$5,027 per Coloradan in 2023 dollars. In 2023, 71% of state spending was exempt, amounting to $8,442 per Coloradan.

- Proposition 117, which requires new enterprises projected to generate revenue above a threshold to receive voter approval, passed in 2020. Since then, the legislature has directly established eight new enterprises and expanded a preexisting one, costing Coloradans a total of $88.3 million in FY23.

- If all Colorado’s fee enterprises, minus higher education, were instead funded by the state income tax, the state income tax would increase to 7.68%, a 75% increase from the current rate of 4.4%.

- Since 2018, voters have approved two income tax cuts worth a combined reduction of .23 of a percentage point. At the same time, fee-based revenue to enterprises has increased by an amount equivalent to a .51 percentage point increase in the state income tax.

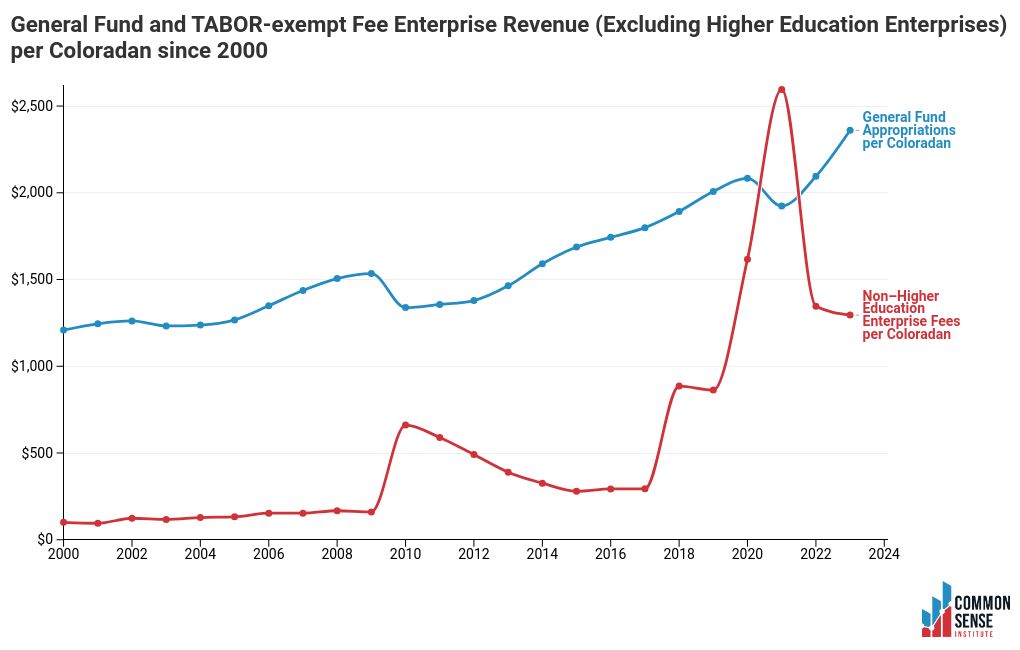

- In 2000, enterprises collected $222 per Coloradan and the General Fund received $1,174 per resident. By 2023, these amounts had grown to $3,791 and $2,360, respectively—for every $1 increase in General Fund revenue per Coloradan since 2008, total fee collections rose by $3.10.

Introduction

TABOR (Taxpayers’ Bill of Rights) was approved by Colorado voters to provide taxpayer protections over the growth rate of government. Lawmakers must secure voter consent to retain tax revenue above its limit.

[i] Governments can still raise new money through fees, however, and have done so liberally in recent years.

Fees have driven Coloradans’ effective tax burdens higher and higher. Over most of the last two decades, fee revenue has grown faster than the state’s General Fund; per Coloradan, it has tripled since 2008 to $23.3 billion in 2023 alone.

In 1996, only 46% of total state spending was TABOR-exempt—$5,027 per Coloradan in 2023 dollars.

In 2023, 71% of state spending was exempt, amounting to $8,442 per Coloradan. There is no reason to expect this trend to abate in the future.

Colorado’s income tax rate is among the lowest in the country, but that fact belies the state’s substantial reliance on fee revenue. If all Colorado’s fee enterprises were instead funded by the state income tax, it would have to grow to 14.41% to accommodate 2023 levels. If higher education enterprises are excluded, the state income tax would still need to increase to 7.68%, a 75% increase from the current rate of 4.4%.

Since 2018, voters have approved two income tax cuts for a combined .23 percentage point reduction. At the same time, fee-based revenue to enterprises has increased by an amount equal to a .51 percentage point increase in the state income tax.[ii]

History of Fees in Colorado

Since the adoption of TABOR in 1992, voters have approved only a handful of statewide tax revenue increases, the majority of which have been “sin taxes” imposed on products such as tobacco and actives including sports betting. While many local governments have received voter approval to retain revenues above the TABOR spending limit, a large share of state revenue and spending is still subject to the limit.

As tax rates have been kept lower by TABOR’s growth limitations, the Colorado legislature has shifted more of the state’s revenue dependence to fee-based enterprises. By 2020, lawmakers had created 24 such enterprises which, together, collected $20.9 billion of revenue in that year. In just three years since then, the total increased to over $23.3 billion.

Even since the 2020 passage of Proposition 117, a direct rebuke of the rapid growth of fee revenue, the legislature has established eight new enterprises and expanded a preexisting one, costing Coloradans a total of $88.3 million in FY23, some of which is not TABOR-exempt.

Why Does the Difference between Taxes and Fees Matter?

TABOR’s provisions apply to state taxes; however, most fees and all federal revenues are exempt. The Colorado government collected fees prior to the enactment of TABOR in 1992, but the proportion of the Colorado state budget comprised of fees increased following its passage, a trend which has continued to the present day.

In 1996, only 46% of the total state spending was TABOR-exempt—$5,027 per Coloradan in 2023 dollars.

In 2023, 71% of state spending was exempt—$8,442 per Coloradan.

How Is Fee Revenue Collected?

Users of public services, like parks, toll roads, and waste disposal facilities, pay fees to the state government enterprises responsible for them. These enterprises are government-owned entities that fund their operations with the fees they collect. They must receive less than 10% of their funding from government grants.

[iii] Some fee enterprises, including several that were established after 2020, provide no direct services to their payers and behave instead as means of generating revenue for government projects and/or disincentivizing adverse behaviors.

2020 Proposition 117

As public consciousness of increasing fee revenue rose, appeals for fee relief did as well. The loudest of these was Proposition 117, a citizen-led initiative which appeared on the 2020 statewide ballot. Proposition 117 proposed requiring voter approval for the creation of any new state enterprise projected to generate more than $100 million in revenue over its first five years. The proposition passed and became law in 2021. As Colorado voters have historically rejected most tax increases, Prop 117 was expected to slow the growth in state fee revenue collection.

Where Do Fees Stand Now?

Data from the three years following the enactment of Proposition 117 demonstrate that fee revenue growth has not declined as expected;

instead, it has grown even more rapidly. In FY23, revenue collected from enterprise fees totaled $23.3 billion, accounting for over half the state budget.

Between 2008 and 2023, the total amount of TABOR-exempt revenue collected by enterprises per Colorado resident tripled and fee revenue grew substantially faster than General Fund revenue. In 2000, enterprises collected $222 per Coloradan and the General Fund received $1,174 per resident. By 2023, these amounts had grown to $3,791 and $2,360, respectively—for every $1 increase in General Fund revenue per Coloradan since 2008, total fee collections rose by $3.10.

Why Has Fee Revenue Continued to Grow?

Most importantly, though the passage of Proposition 117 required voter approval for the creation of large new enterprises, it did not restrict the growth of existing enterprises. Revenue collected by almost every enterprise active in 2020 has continued to grow unimpeded.

Additionally, the Colorado General Assembly has exempted several revenue sources from the TABOR cap by designating them as state enterprises. The largest of these is public university tuition and fees, which was reclassified in 2005. Even this, however, is not primarily responsible for the long-term growth of fee revenue—excluding higher education fees, total enterprise revenue grew from $97 per Coloradan in 2000 to $1,295 in 2023.

Lastly, the proliferation of new enterprises since the passage of Proposition 117 appears to be accelerating fee revenue growth. Eight new enterprises have been constituted since Proposition 117 became law, which is far more than have historically been established over similar periods of time. Fees under one preexisting enterprise, the Bridge and Tunnel Enterprise, have been substantially increased as well.

Of the eight new enterprises, all were established by the state legislature without being referred to the ballot to assess their popularity with voters.

[1] The collections of these eight are comparable to those of many established funds. The largest new enterprise collected $19.4 million in 2023 and the eight together collected a total of $65 million, most of which came from non–TABOR-exempt fees imposed by a single bill (SB21-260).

[iv]

Looking Forward

Two major pieces of fee-related legislation were passed into law during the 2024 legislative session and will take effect in the coming years. SB24-184 imposes a fee on vehicle rentals to create the Transportation Enterprise Special Revenue Fund, with a projected revenue of $28.5 million next year.

[v] SB24-230 establishes fees on oil and gas production in the estimated amount of $109.4 million next year to benefit two existing enterprises: the Clean Transit Enterprise and the Colorado Parks and Wildlife Enterprise.

[vi]

Bottom Line

The more that fee increases assume the character of tax increases, especially in the aftermath of Proposition 117, the more appropriate it becomes to characterize them as such. The comparative difficulty of enacting tax increases in Colorado has for decades encouraged lawmakers to instead use fees as means of generating new revenue for the state; the evidence of the years since 2020 suggests that Proposition 117 drove them only to change tactic, not change course. Fee revenue growth, therefore, is still driving Coloradans’ effective tax burdens higher and higher without giving them a say in the process—far beyond levels that they’d likely approve on a ballot. \

[1] Note: The Family Medical Leave Insurance Enterprise was approved on the 2020 ballot alongside Proposition 117.

[i] https://leg.colorado.gov/agencies/legislative-council-staff/tabor

[ii] https://commonsenseinstituteco.org/proposition-117/

[iii] https://www.sos.state.co.us/pubs/info_center/laws/COConstitution/ArticleXSection20.html

[iv] https://leg.colorado.gov/sites/default/files/documents/2021A/bills/fn/2021a_sb260_f1.pdf

[v] https://leg.colorado.gov/sites/default/files/documents/2024A/bills/fn/2024a_sb184_r2.pdf

[vi] https://leg.colorado.gov/sites/default/files/documents/2024A/bills/fn/2024a_sb230_00.pdf