Introduction

Colorado’s public education system continues to suffer from a protracted COVID-19 hangover. While student performance as measured by standardized test scores has returned to pre-pandemic levels, enrollment, which plunged precipitously during the pandemic, continues to decline from that low point. Achievement stagnation and enrollment drops are lingering impacts of decisions to close schools to in-person learning for extended periods of time in 2020 and 2021.

Colorado public schools continue to benefit from federal, state, and local largesse, though the massive federal infusion of dollars in the wake of COVID-19 ended this past summer. Over time, however, that loss will be more than compensated for by the General Assembly’s elimination of the Budget Stabilization Factor during the 2024 legislative session. It becomes ever harder to argue convincingly that Colorado’s public schools are underfunded, especially as they continue to underperform. Since 2020, total public education revenue from all sources has climbed 14.3% from $14.5 billion to $16.6 billion while total expenditures have climbed 21% from $14.6 to $17.7 billion.

At the same time, student enrollment steadily declined for many districts and is forecasted to keep sliding downward for the foreseeable future. In 2023–24, statewide public-school enrollment was almost 32,000 students below its 2020 peak—a drop of 3.5%. The combination of funding increases and student decreases has meant that total expenditures per student going to instruction and support increased by 35% since 2018, growing from $11,248 to $15,208.

Student achievement, as reflected in the Colorado Measures of Academic Success (CMAS) results, has finally recovered from significant declines in the immediate aftermath of the pandemic. Still, this only places achievement back at square one rather than in positive territory. Third-grade reading and math proficiency rates only this year returned to pre-pandemic levels.

Each year, the Colorado Department of Education releases a new set of data on the finances of Colorado’s PreK–12 public education system. This report summarizes several different dimensions of the financial data and shows key trends in how education funding and spending have changed over time.

Key Findings

While federal funding, which grew in the wake of the COVID-19 pandemic, has dropped from its peak, it still makes up a larger share of total Colorado education funding than it did before the pandemic—local and state revenue increases have more than made up for the loss anyway, despite continued enrollment drops. As in years past, increased spending has not moved the needle much on student learning as measured by standardized test scores and the trend of disproportionate spending on administration rather than instruction and student support continued last year.

Colorado K-12 enrollment has dropped for four consecutive years.

- After a steep drop of more than 30,000 students in one year during the pandemic (2021), public-school enrollment fell by another 5,053 students between 2022 and 2024. Before the pandemic, statewide enrollment had not declined in any single year since 1989.

- PreK–12 enrollment declines were spread across the state, except the northeast region, which gained 1,164 students (6.5%). Since 2020, enrollment in the northeast has grown by 28.9%. During that same period, southeast enrollment dropped by 12.4%, and the metro region, where the majority of students reside, lost 6.6% of its student population.

- Since 2020, grades PreK–9 have fallen in population while enrollment in grades 10–12 has grown modestly.

Public education funding keeps rising, even as enrollment drops.

- Public education revenue is largely determined by the funded pupil count, rather than enrollment. The funded pupil count includes averages of prior-year trends, so it has not declined at the same speed as total enrollment. Between 2020 and 2023, the funded count fell by 1.9% while total enrollment dropped by 3.3%.

- Total revenue per funded student from state, local, and federal sources grew to $17,666 in FY23—20% above 2020 levels. Funding from other sources such as bond proceeds added $1,188 in funding per student.

- Federal funding as a percentage of total education spending peaked in 2021 at 12% then declined for two consecutive years to 9.1%. That figure, however, remains significantly higher than pre-pandemic levels. Federal funding comprised just 5.9% of Colorado education spending in 2019.

- State revenue continues to provide greater shares of total education revenue in poorer, more rural regions of the state. This illustrates the impact of low property tax rates and/or property values in these areas.

Education spending continues to disproportionately prioritize administrative and non-instructional categories while student achievement remains largely flat.

- Total education expenditure grew to $17.65 billion in 2023, an all-time high. That is an increase of $1.64 billion since 2022 (10.2%) and an increase of $4.68 billion (36%) since 2018. Instruction and support expenditure totaled $13.37 billion in 2023, an increase of $1.13 billion (9.3%) since 2022.

- The share of spending on instruction shrank over the last five years from 41.4% in 2018 to 40.1% in 2023. The share of spending on support grew over that same period from 33.9% to 36%.

- Instructional salaries and benefits, however, remain the largest expenditure categories in all regions of the state except the northeast, where the “other expenditures” category exceeds salaries and benefits.

- Staff head counts over the past 15 years reflect a shift in school staffing strategies in favor of more non-teacher instruction and support staff. From 2009 to 2024, teacher headcount increased 10% while student population increased 8%. During the same time, the number of administrators grew 26% and non-teacher instruction and support staff grew 29%. (Figure 1). These groups soared even as the student population dipped over the past four years.

- Enrollment growth has fallen behind that of every staff category, especially support staff and district administrators. The number of administrators nosedived in 2020 and 2021, presumably because of the pandemic, but has grown faster than all other categories since then.

- The gap between teacher salary growth and overall spending growth continues to widen. Since 2007, overall funding per student grew by 69%, while the average teacher salary grew by 50% (Figure 2). This is a narrower gap than in previous years, but it remains notable.

- Student outcomes have not kept pace with spending increases. Third-grade reading and math proficiency rates only this year returned to pre-pandemic levels.

Figure 1

Figure 2

The fact that teacher salaries have risen at a rate significantly slower than education funding raises questions about school districts’ spending priorities. As student achievement continues to stagnate, these dollar figures suggest that instruction has not been the top priority.

Part 1: Enrollment

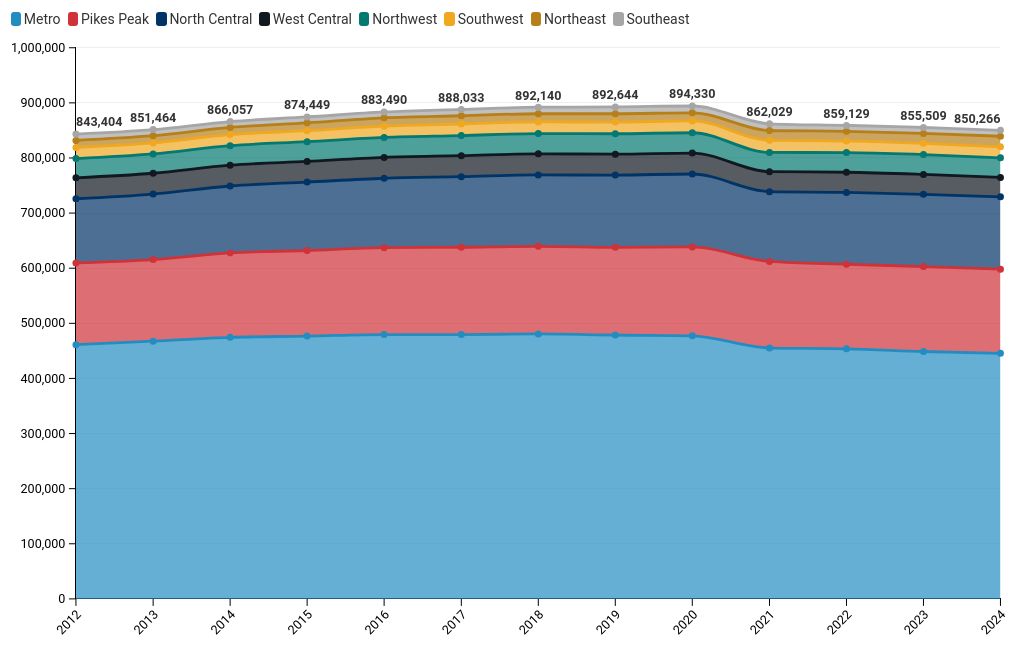

Figure 3: Colorado K–12 enrollment over time

Colorado’s K–12 enrollment has now fallen for four straight years. The decline’s persistence, at this point, suggests that there are demographic and perhaps parental satisfaction issues at play. While the COVID-19 pandemic led to a steep drop between 2020 and 2021, the continued decline cannot be explained by the pandemic alone, though there’s some evidence that Colorado’s school-age population is falling overall.

The northeast and north-central regions have bucked this trend, showing slow and steady annual growth since the pandemic. Most of the enrollment decline has come from the Denver metro region, which has lost 6.7% of its student population since 2020—from 477,355 to 445,611.

Declining enrollment is also an issue among younger children. Enrollment has increased since 2020 only in grades 10–12, which implies that the statewide decline has mostly been caused by departures of young students and decreased enrollment of kids reaching school age. Steep enrollment declines in the earliest grades continued in 2024 (down 6.9% in pre-K and 8.4% in kindergarten compared to 2020) even as the state has expanded K and pre-K funding. As these enrollment declines roll up through the grade levels, overall drops in enrollment could look increasingly pronounced.

Figure 4: PreK–12 Enrollment by region

Figure 5: Enrollment changes by region between the 2020 and 2024 school years

Only the northeast region’s enrollment is higher now than it was in 2020. Notably, the northeast is the second-smallest region by enrollment, spends the second-least per pupil on instruction and support, has the lowest graduation rate, and pays its teachers the least.

Figure 6: Enrollment changes by grade between the 2020 and 2024 school years

High school enrollment was least affected by the pandemic, but other grades’ declines are starting to filter through. Last year, the ninth-grade bar was blue and next year, the 10th-grade bar is likely to turn red.

Part 2: Revenue

Public K–12 revenue comes from four main funding sources: local, state, federal, and other. Local revenue comes from property tax, specific ownership tax, and other funds produced within a school district for public education. This category includes mill levy overrides and mills for bonded indebtedness. State revenue includes all funds collected by the state government that are appropriated to school districts, including per-pupil funding from the State Education Fund, program funding, and other state grants and projects. Federal revenue is any money distributed to the school district from the federal government, whether directly or through an intervening agency like the Colorado Department of Education.

Federal dollars typically require specific spending. Federal funding, for example, is used to support educational services for students with disabilities and English language learners and to fund programs at districts and schools that have large numbers of low-income students.

Figure 7: History of total revenue (including other sources)

Figure 7 shows that Colorado school funding is continuing to rise roughly in line with its 10-year history, despite four straight years of declining enrollment. In large part because of a massive federal infusion of dollars, the pandemic does not appear to have produced a long-term funding shortfall. That funding has ended, however, and districts faced a September 30 deadline for spending or obligating those dollars. The last of the impact is likely to appear in next year’s data. Some of that loss will be offset by the state’s elimination of the budget stabilization factor during the 2024 legislative session. Total state and local funding for public schools is projected to increase by more than $500 million and the state share of total program funding will rise to $9.7 billion.

Figure 8: Major revenue sources for K–12 public education as shares of total (excluding other sources)

As Figure 8 shows, the federal share of district revenue is still inflated due to the U.S. government’s response to the pandemic but is gradually trending back toward historical norms.

Figure 9: Local, state, and federal revenue as shares of total revenue by region

Figure 9 provides a sense of how reliant each region is on local revenue (from property taxes) and the statewide school funding formula. A large red bar indicates either relatively low property tax rates or low property values.

There are significant regional variations in the relative distribution of local, state, and federal funds to school districts. The rural southeast region receives the lowest share of local funding, presumably due to stagnant property tax growth. With the exception of the non-geographical Charter School Institute, the local share of regional revenue is a strong indicator of the relative wealth of the regions’ school districts.

Part 3: Expenditures

Figure 10: Total Annual Public Education Expenditures

Public education expenditures generally fall into the following categories: instructional services (staff salaries and benefits, supplies and materials, purchased services, capital outlays, and other) and support services (district and school administration, operations and maintenance, pupil transportation, food services, and “other”).

Once again, in 2023, public education spending hit its highest level ever in Colorado, at $17.7 billion. The share of spending on instruction has fallen in the last 10 years while spending on support services has risen.

In 2023, instructional services accounted for 40.1% of total spending, while support services comprised 36%, and other spending accounted for the remaining 23.9%. The Colorado Department of Education’s definition of “other expenditures” is “amounts paid for all expenditures other than instruction, support services, and community services.”

The state defines enrollment as the straightforward student headcount. The funded pupil count, which controls how much funding schools receive through the School Finance Act, is determined by a formula based on current enrollment and previous years’ enrollment trends. The formula guarantees that the funded pupil count declines at a slower rate than the headcount during periods of falling enrollment, presumably to help prevent underfunding struggling schools.

Between 2022 and 2023, total public education spending grew by more ($1.6 billion) than it has in any single year for which data are available, despite falling enrollment. Some of this is attributable to higher-than-normal inflation, but inflation in the 2022 calendar year was only about half of what it was in 2021.

Figure 11: Shares of major expenditures in public education

Figure 12: Growth in enrollment, funded pupil counts, and classroom expenditure since 2007

Between 2009 and 2023, inflation-adjusted instruction and support expenditure grew by 26.4% while the funded pupil count increased by only 16%. Spending rose especially sharply in 2023, even though the funded pupil count, which affects state funding, declined by more than ever before; as a result, the difference between the two growth rates is now higher than it’s been at any point across the scope of Figure 12. In 2023, enrollment was the lowest it had been since 2014; since 2020, when enrollment was at its peak, inflation-adjusted spending on instruction and support has increased by 3.7% while PK-12 enrollment has declined by 3.3%.

The sudden spike in the funded pupil count between 2019 and 2020 occurred because preschoolers were added to the formula in 2020.

Figure 13: History of total expenditures by region

Figure 13 illustrates total expenditures by region for three years. Significant jumps in expenditures between 2018 and 2022 reflect the infusion of COVID-19 relief dollars, which should drop away next year but could be offset by increased state spending. Spending has trended consistently upwards in every region across the last 10 years. Over that period, it has at least doubled among charter schools and in north central, northeast, and southeast regions.

Figure 14: Instruction and support expenditures per pupil by region

Figure 14 illustrates per-pupil spending on instruction and support by region for three years: 2013, 2018, and 2023. Figure 15 provides a more granular look at spending by region in 2023. Variations by region are modest. Once again, federal COVID-19 relief funds are reflected in big spending increases between 2018 and 2023.

- The largest share of the metro region’s instruction/support spending goes to teacher salaries and benefits.

- Rural districts devote large shares of their instruction/support spending to matters other than compensation and direct student/staff support, largely due to especially high transportation and material costs.

- Average spending levels across the state’s eight regions generally correspond to their reliance on local revenue (an effective proxy for relative affluence). The southeast region is notable for spending the second-most on instruction and support per student in 2023 despite spending only the seventh-most in 2018.

Figure 15: Regional shares of total instructional and support expenditure by category in 2023

Figure 16: Statewide shares of total expenditure by instructional/support category

Figure 16 shows that, though instructional salaries are generally rising, they have become smaller shares of spending over the past decade. This indicates the potential for some crowding-out by spending priorities like administration and operations, both of which occupy larger shares of district budgets than they did previously. If the same shares of districts’ budgets were spent on instructional salaries now as in 2013, teachers would be receiving $15,908 more per FTE.

Part 4: Teacher salaries and turnover

Figure 17: Average regional teacher salaries over time

Statewide, the average salary reached $63,224 in 2023, an increase of 20% since 2018. There remain significant disparities by region: The average teacher salary in the southeast was $45,135 (up 18% since 2018), while in the metro region, it reached $70,164 (up 21.3%). In general, salaries have grown at lower rates in regions with lower absolute averages.

Figure 18: Average teacher salaries and turnover rate in the metro region

The scatter plot in Figure 18 shows that teacher turnover in the metro region is negatively correlated with average pay. In the Boulder Valley school district, where the average salary is over $95,064, teacher turnover was just 12.4%. In the semi-rural Clear Creek school district, where average pay is $59,383, turnover was 27.3%.

Figure 19: Average education staff turnover rates compared to other industries

Despite much angst over teacher turnover, the fact remains that turnover is much lower among public education workers in Colorado than it is in most other industries. This may be because education jobs generally offer more stability and less mobility than private-sector jobs. Turnover among public education workers has declined recently, too: after spiking to 19.1% last year, teacher turnover in Colorado dropped back down to 17.3% in FY24.

Part 5: Student performance

Figure 20: Four- and six-year graduation rates in Colorado

Other than a brief backslide in 2021, probably associated with the pandemic, graduation rates continue to tick upward across the state.

Figure 21: Four-year high school graduation rates by region (2023)

Colorado’s graduation rate is measured by how many students enter the ninth grade and progress through 12th grade, completing all academic requirements, in either four or six years. Colorado’s four- and six-year high school graduation rates have risen slowly but steadily over time.

Colorado’s four-year graduation rate continues to rise steadily, having reached an all-time high of 83.1% in 2023. The six-year graduation rate in 2021 (the most recent available) dropped by four-tenths of a percentage point from the previous year but remains near historical highs. There remain significant regional disparities between the best- and worst-performing regions, across which there appears to be a moderate correlation between graduation rates and instruction/support spending per pupil.

It is worth noting, however, that state academic standards are not well-aligned to college readiness standards or workforce readiness standards, bringing into question the value of a Colorado high school diploma.

Figure 22: Third-grade reading and math proficiency rates

Statewide third-grade reading and math scores in 2024 finally exceeded pre-pandemic levels after previously stagnating or declining since 2019. While this is notable, it is hardly cause for celebration that over half of the state’s third-graders unable to read, write, or perform basic math at grade level. Research shows that students not reading proficiently by the end of third grade face major problems ever catching up.

Figure 23: Third-grade reading and math proficiency rates by free or reduced-price lunch eligibility

Achievement gaps between low-income and more affluent students improved slightly in 2024, though they have widened since the pandemic from 29.6 to 32.6 percentage points in math and from 30.1 to 31 percentage points in English language arts.

Conclusion

Public education in Colorado continues to underperform as its funding levels increase and its enrollment falls. Although standardized test scores have at last returned to and even slightly surpassed pre-pandemic levels, troubling achievement gaps and low proficiency rates persist. The elimination of the state’s Budget Stabilization Factor means that, even though federal pandemic relief funding has ended, the rapid increase in education funding that began five years ago will continue. Colorado taxpayers might reasonably wonder whether they’re benefitting from this largesse and demand better from the state’s public-school districts.